Gulke: Agricultural Positioning

The views expressed are those of the individual author and not necessarily those of DTN, its management or employees.

(Charts by Gulke Group)

Two weeks ago, I flagged some concerns in January 2027 soybeans. Prices had gone sideways for roughly six weeks, posting reversals in both directions without extending meaningfully either way. That changed on April 30/May 1, when the market closed above the March highs to end April and begin May — and then extended further. The trade has clearly turned to new-crop soybeans as the leader.

Last week, I focused again on the idea of food as a strategic national concern, citing wheat as a prime example. Finally, after months of suggesting that such a concern should be evolving, I was pleased to hear the ag announcer on an ag radio show on Tuesday, suggesting this very same thing. It has taken a while to sink in, but the energy situation globally is likely stirring interest. Food is much more of a concern than oil, I would think.

I have often written that the market’s job is price discovery — particularly forward-looking price discovery. By the time an anticipated development shows up in the media, the market may have already priced it in. That appears to be the case for old-crop commodities right now, though it may not be true yet for new-crop 2026.

If you look at the price action (technical analysis), old-crop corn, soybeans and wheat filled some objectives, with July soybeans filling — but not closing above — the down gap posted on March 16.

July corn touched the exact high posted in March but failed and closed lower. July wheat failed last week at an attempt at new highs over March and posted a daily key reversal lower on Tuesday, as well as teasing with a longer-term negative action after crop ratings said deterioration may be over.

The action is in new-crop pricing, which, while lower, was not severe and continued to hold over previous 2026 highs. Call it trader-spreading or some other reason the media may find as an excuse, including the proverbial “turnaround Tuesday.” Whatever one wants to assume, there was, in fact, action that warrants concern; the timing is right, as things anticipated in this column are now being noticed.

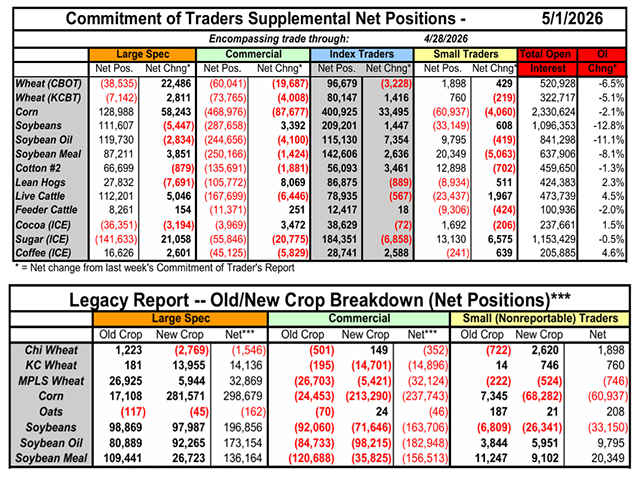

One final observation regarding the large spec report last Friday: There was a huge increase in net-long positions in corn (and a big move in new crop — see the legacy report). In soybeans, net-long positions in old crop declined slightly while new-crop net longs increased sharply (again, see the legacy report). Chicago wheat could not muster a net long, while KC and Minneapolis (premium wheats) are net long new crop. See the large spec tables accompanying this week’s column for more details.

Media commentary often treats a large net-long speculative position as a warning sign, implying that large specs will eventually sell. As so often has been the case in the past, a spec gets long for a reason and can stay that way long after a novice in the business has run out of margin money shorting the market. The reverse holds equally true: as noted last week, spec traders have remained net short in wheat for years at a stretch. When a large spec finally reverses a long-held position, that is the signal worth watching.

I consider what is happening in old crops and the attention to the new crop in keeping with my outlook for a paradigm shift in ag that began 18-19 months ago. Long-term, however, it can take a while. In the meantime, let volatility and price confusion separate the wheat from the chaff in the marketplace.

Jerry Gulke can be reached at (707) 365-0601 or by email at Jerry@gulkegroup.com

(c) Copyright 2026 DTN, LLC. All rights reserved.