Gulke: Xi-Trump Summit Repercussions

The views expressed are those of the individual author and not necessarily those of DTN, its management or employees.

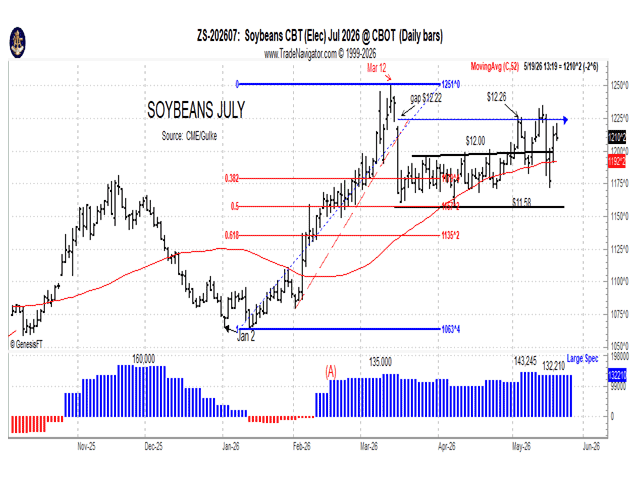

This July 2026 soybean futures chart reflects some important points in the price-discovery process since Jan. 2, 2026. (Chart by Gulke Group)

Last week, I concluded that the paradigm shift in the way we will do global ag business, which started in August 2024, was still ongoing. The results of last week’s meeting between Chinese President Xi Jinping and U.S. President Donald Trump appear to have given it new meaning.

Also, over the months, in this column and in media interviews, I suggested that for China to buy soybeans from the U.S. at a value of, say, $1 per bushel higher than from Brazil, it was an investment not an expense. The theory was that China would basically gain more in lifted tariffs than the extra cost of soybeans.

While Trump stated that tariffs were not on the agenda, Chinese newswires reported that there were discussions on tariffs — especially the 10% tariff on Chinese goods scheduled to expire in June — not being reinstated. The art of the deal!

The trade viewed the surprise announcement of the $17 billion agreed-upon purchase of other ag products as bullish. More likely, it caught bears unaware, and they ran for the exits. Reportedly, open interest and volume were weak on the rally on Monday. In fact, they were weaker than the move higher that peaked prices on March 12.

Some bullet points regarding the newest agreement between the U.S. and China are as follows and are subject to change as more documentation is revealed.

— It appears that any formal signed agreement will happen when President Xi from China comes to visit the U.S. in September.

— The two countries are creating a U.S.-China Board of Trade (or, as China calls it, a Trade and Investment Council) to address and maintain this agreement on an ongoing basis. It appears that this is in place instead of creating hard penalties within the agreement that could essentially nullify it.

— On the agricultural side, China has agreed to buy 17 billion dollars’ worth of agricultural goods in 2027 and 2028. A prorated amount of about $8 billion will be in place for 2026.

— This $17 billion commitment is said to be stacked on top of/separate from the already agreed-upon purchases of 25 million metric tons (mmt) of soybeans in 2026, 2027 and 2028. What this means is that China will spend roughly $25 billion to $30 billion worth of agricultural products, which will bring China’s purchases back to near normal levels.

A closer look at the agreement:

— The overall agreement has a one-year trade truce framework applied to it. Although this has been touted as a three-year deal, it has been suggested that it will be reviewed on a yearly basis.

— There appears to be an abundance of out clauses regarding the whole agreement. But on the ag side, there are included items like sanitary and phytosanitary concerns and non-compliance of agreed-upon tariff reductions.

— Currently, there has been no talk regarding any out clauses due to market prices, commercial demand, etc., like were in the Phase One deal of Trump I.

— On the surface, if there is any reason to dissolve this agreement, it does not affect the previously agreed-upon 25-mmt soybean purchase.

PRICE DISCOVERY

The July 2026 soybean chart accompanying this week’s column reflects some important points in the price-discovery process since Jan. 2, 2026.

The rally to March 12 and subsequent swift 70-cent hit on soybeans is obvious, including the price gap lower the following Monday, March 16. Price tried to rally and post in the highs over Mar during April and again during early May but failed. It tried again this week.

The question to be answered is whether the revelation of the new trade agreement is more consequential (bullish) than what was anticipated during the first 10 weeks of 2026. During that time, there was anticipation of such a meeting between the two countries that was announced but then put off due to the Iranian skirmish.

The post-March 12 collapse caught support right at 50% of the total move from Jan. 2 to March 12. Coincidence? I think not!

The $12 level is significant, not only from a psychological point of view, but as the level at which the price exploded through Sunday night.

A lot is at stake in the next few days, and certainly by Monday morning. Should prices again fail to exceed and sustain a level above new highs for May, the handwriting would likely be on the wall. After such a long time promoting the positive outlook for soybeans — especially since Jan. 2 against a backdrop of record production out of Brazil — it would be a classic market where all the doubters got bullish at the top, if it were not for the relentless large spec and his desire to be net long during the period of disillusionment.

Media folks will be touting that the large spec will have to sell sometime. The question is, will he do it now or stay long through the summer, waiting for China to buy next fall?

Technical analysis was proactive on Jan. 2 and for 15 months prior. I suspect it will lead the way again. The fact that the jump in prices appeared to be lacking in volume does concern me.

Jerry Gulke can be reached at (707) 365-0601 or by email at Jerry@gulkegroup.com

(c) Copyright 2026 DTN, LLC. All rights reserved.