Gulke: Is Food a Strategic Concern?

The views expressed are those of the individual author and not necessarily those of DTN, its management or employees.

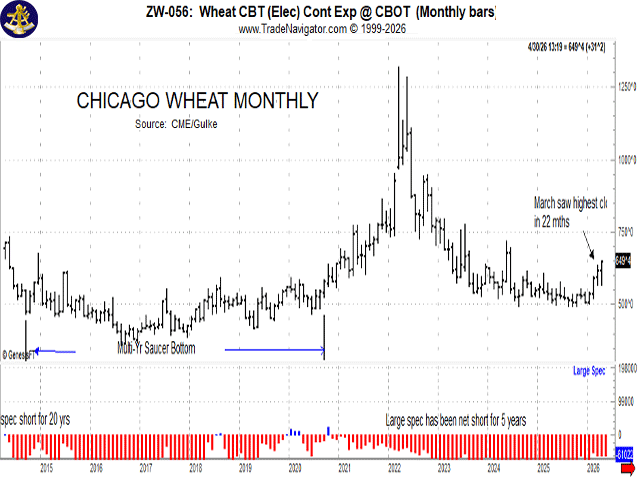

Given the concerns regarding the cost and availability of fertilizers and the U.S. wheat crop concerns, it is no wonder that the large spec (shown in red bars) has been trimming his net-short positions recently after being largely net short for decades. (Chart by Gulke Group)

It appears that media attention on commodities has begun to take hold. This comes after I discussed in this column 18 months ago that a paradigm shift was materializing in the way we are going to do ag business going forward. The lack of recognition of what was going on in the background was rather taxing, but with the acceleration in wheat futures this week, perhaps a new day is dawning?

Wheat, as the monthly Chicago wheat chart accompanying this week’s column reflects, doesn’t get much respect from a global perspective. We are basically a small fish in a big pond. For example, for the 2023-24 wheat year, the U.S. produced approximately 46.3 million metric tons (mmt) of all wheat. The EU produced 140.5 mmt — nearly three times as much as the U.S. during the same period. In fact, adding all other major producers — Russia, Australia, Argentina, Canada and China — global wheat production, including in the U.S., was about 789.8 mmt. It is easy to see why we become the residual supplier and get the brunt of low prices, as a 10% deviation in our crop is peanuts compared to the global supply.

But there is some good news. If/when one of the big players like the EU or Russia (at 85 mmt) has a hiccup, other producers must take up the slack if the production reduction is significant. Earlier this year, wheat stocks were estimated to end up being about 850 million bushels (mb). It takes getting U.S. stocks to around 500 mb for things to get dicey and for there to be a meaningful price response. That is only about a drop of 8 mmt to 10 mmt of global supply, or less than an 8% reduction in the EU production.

Given the concerns regarding the cost and availability of fertilizers and the U.S. wheat crop concerns, it is no wonder that the large spec (shown in red bars in the accompanying chart) has been trimming his net-short positions recently after being largely net short for decades. If the large spec were to get net long upon the release of any weekly update of the CFTC positions, it would add to my evolving paradigm shift scenario.

This week, on Monday and Tuesday, wheat prices saw significant movement, culminating in Tuesday’s large move of 30 cents at one time. One can only imagine what the psychological effect of traders would be like if the CFTC shows that the large spec could finally bring him/herself to getting net long wheat.

Wheat is produced by nearly every country in the world. Some don’t produce enough. Some, like those mentioned above, produce too much. When a large net exporter has less to support, global markets get concerned.

I have mentioned previously the importance for importing countries to recognize the need for strategic reserves of grains. If energy is strategic, when will the light come on to recognize that food and fiber is even more important in our new eco-political atmosphere?

It continues to amaze me, after decades of analyzing markets, that technical action often predicts months in advance what the fundamentals finally reveal. Funny how that works.

I’ve said it before: Most market observers wouldn’t recognize a bull market if they saw it walking down the street. It was missed 18 months ago. Wouldn’t it be nice if we were just getting started?

Jerry Gulke can be reached at (707) 365-0601 or by email at Jerry@gulkegroup.com

(c) Copyright 2026 DTN, LLC. All rights reserved.