Gulke: Ag’s Paradigm Shift Continues

The views expressed are those of the individual author and not necessarily those of DTN, its management or employees.

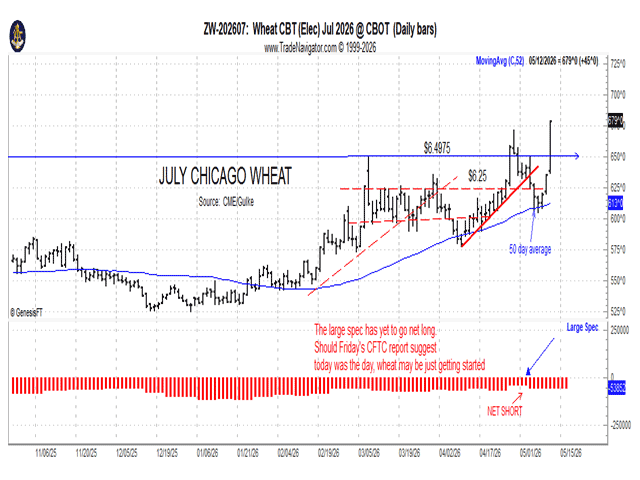

(Chart by Gulke Group)

It is not often that we get positive price responses to the May WASDE report. Tuesday was a pleasant exception. Using the front-month continuous futures contract, prices peaked last year on Feb. 21 and didn’t get higher until after the marketing year was completed. For corn and soybeans, that was Aug. 31. Prior to that, prices tended to top around May 12 for corn and June 10-12 for soybeans; wheat has a different marketing year, so it’s not as comparable to corn or soybeans.

Starting on Jan. 2 this year, the media was generally expecting a repeat of last year for the mid-February highs. But the shift in outlook beginning Aug. 31, 2024, suggested times were changing, and a new paradigm shift in ag outlook was underway. It has taken an 18- to 19-month process to evolve, with the May 12 report presenting a line in the sand. Will the long-term upward bias continue, or will it stall out?

WHEAT: Tuesday’s report supported grains further on fundamental news of the paradigm shift that was predicted months ago but had not yet played out. Wheat was the most obvious, finally responding to the long two-year base-building timeframe of low prices. Actually, wheat posted a longer-term technical buy signal in April 2024, but it took that long to evolve with reasons fundamental longer term in the WASDE report on U.S. production shortfall. U.S. wheat production is a small fish in the big pond of global production, but should one or more major exporters have a production problem, it will add to the excitement that has already started.

CORN: Corn’s lead contract is now 80 cents higher than that Aug low of $3.97m or about $160 per acre. Fundamentally, the WASDE report put the 2026-27 carryover at 1.957 billion bushels versus this year’s 2025-26 at 2.142 bb versus about 1.55 bb for 2024-25. Think about it: We carried into a new-crop year 600,000,000 million more corn into the new 2025-26 marketing year, and demand (exports especially) is up nearly 500,000,000 but disappearing the excess production. If that isn’t a paradigm shift, I don’t know what is. And next year’s exports aren’t expected to drop much at all. In fact, to balance supply and demand, odds are that exports need to be reduced. A million acres less planted than estimated makes things tighter yet. Add in year-round E15, and things look brighter yet for the long term.

SOYBEANS: Three years ago, the media hype was that if we could utilize biodiesel (veggie-type), we would not be able to produce enough soybeans to meet the soy oil feedstocks needed. Now we are at a point where we need another million acres of soybeans (53 mb) AND canola oil AND used cooking oil (UKO) to meet the veggie diesel feedstocks necessary to meet the ambitious biofuel mandates. Soybeans are now higher by about $3/bu than they were at the start of the paradigm shift in August 2024.

LINE IN THE SAND. Prices in May need to hold onto new highs over Mar/Apr in order to suggest that prices are going to recover more to help the sustainability of agriculture. The meeting later this week in China will provide insight. If there is a concern, it is that another framework will be just that — a framework or memo of understanding and disappointing to the expectations seen in the marketplace. Six to nine months ago — and certainly not in August 2024 — such expectations were voiced in none other than this DTN column, and now we are here. Expectations are high, and I am even hearing in the media the term “food security” as an issue. The futures market being just that, a futures market, the only sustainability I am concerned about is the realization that the importance of food security and of the need to adjust the cost of the raw materials that go into the food chain are long overdue. Let’s hope the progress of the last 18 months predicted by market action doesn’t get derailed.

Jerry Gulke can be reached at (707) 365-0601 or by email at Jerry@gulkegroup.com

(c) Copyright 2026 DTN, LLC. All rights reserved.