Gulke: Confusion Reigns

The views expressed are those of the individual author and not necessarily those of DTN, its management or employees.

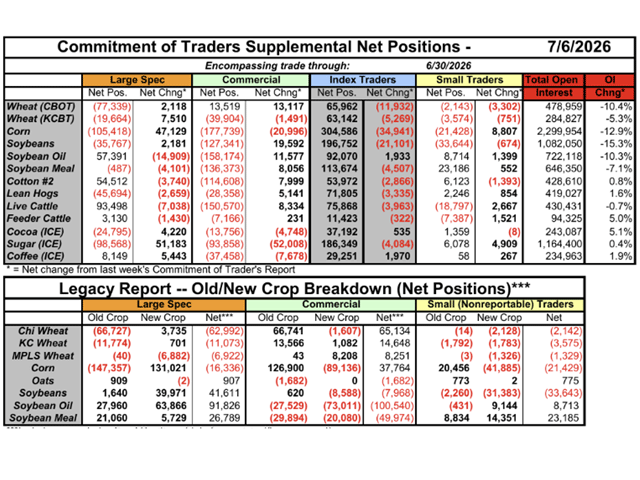

Even the large spec trader got out over his skis and is retracting lessening his short positions while still favoring new crop positive bias. (Chart by Gulke Group)

Last week’s column dwelled on the good news out of the June 30 stocks and acreage reports. Apparently, I was the only one who saw through the report and into the background trading that had been influencing pricing, beginning a couple weeks prior around June 15. I felt the upside risk was greater than the downside price risk. There were nonfundamental indicators supporting that theory.

In fact, my expectations for the report led me to exit hedges — going from 100% hedged to less than 15% two weeks ago in soybeans and to zero coverage in corn. Then I bought upside call options for anticipated use to cover further cash sales if so desired. That recommendation was transmitted to clients as well. See last week’s column for details.

As of Tuesday, corn closed 13 to 17 cents higher and soybeans nearly 70 cents higher than the June 15 period — even more impressive if one uses June 30 as the low. This is about $30 per acre gain for corn and $35 per acre gain on that production. That pays for a lot of those ridiculously high input prices the ag media has been touting. If nothing else, the added gains through marketing flexibility were beneficial. Now the decision of when to capture gains on the recent rally.

So far soybeans have blown through my first upside price objectives. Initial selling by the bears who saw no merit in China buying from the U.S., only to be made a fool of Tuesday on rumors of sales of soybeans to China. Corn is gaining steam as well, as those negative about our ag economic outlook find themselves short-bought and searching for product. The producer who held grains on-farm seems now to be the intelligent one. No doubt the reason why he owns the land and speculators, brokers, and some advisers do not. It makes a big difference if one has skin in the game.

So now the media hype is centered on the weather as being the cause for the recent explosion in prices. But that smacks of an excuse for missing the reversal last week, two weeks after this column stated my urgency to cover short positions before a weather market was even printed.

All this excuse mongering and referencing the big crop in Brazil– which every trader knew about months ago — along with the understanding that China would look at buying soybeans at a premium to Brazil as an investment, not and expense. Knowing and understanding how to make a deal may be wishful thinking on some specs, algorithm traders and AI itself. Common sense seems to illude some seeking to advise producers as the new paradigm shift seen emerging 22 months ago seems alive and well.

Perhaps I am seen as too critical of the musings in the media that erroneously hype certain events. Almost to the extent some seem to be disappointed even that China is buying soybeans from both of our ports, as doing such makes fools out of those who were doubters — especially regarding price discovery and deal making. I have never seen such confusion expressed in the media by commodity market makers, including the stock markets; take a look at the S&P 500 index for example.

In commodities, see the January chart accompanying this column. It caught the bulls positive at the recent top on May 13 and bearish at the bottom on June 30. I expect more to come. The experienced trader calls such action, “shaking the loose leaves off the tree.” It took six weeks in a down market to scare some out. It may take another six weeks to right their ship just in time for the August WASDE!!!

Jerry Gulke can be reached at (707) 365-0601 or by email at Jerry@gulkegroup.com

(c) Copyright 2026 DTN, LLC. All rights reserved.